An overview of market shaping in global health: Landscape, new developments, and gaps

Editorial note

This report is a “shallow” investigation, as described here, and was commissioned by GiveWell and produced by Rethink Priorities from February to April 2023. We revised this report for publication. GiveWell does not necessarily endorse our conclusions, nor do the organizations represented by those who were interviewed.

The primary focus of the report is to provide an overview of market shaping in global health. We describe how market shaping is typically used, its recent track record, and ongoing gaps in its implementation. We also spotlight two specific market shaping approaches (pooled procurement and subscription models). Our research involved reviewing the scientific and gray literature and speaking to five experts.

We don’t intend this report to be Rethink Priorities’ final word on market shaping, and we have tried to flag major sources of uncertainty in the report. We hope this report galvanizes a productive conversation within the global health and development community about the role of market shaping in improving global health. We are open to revising our views as more information is uncovered.

Key takeaways

- Market shaping — in the context of global health — comprises interventions to create well-functioning markets through improving specific market outcomes (e.g., availability of products) with the end goal of improving public health. Market shaping interventions tend to be catalytic, timebound, and have a strong focus on influencing buyer and supplier interactions. [more]

- Market shaping interventions are used to address various market shortcomings. A commonly used framework to assess shortcomings in various market characteristics is some variation of the “five As”: affordability, availability, assured quality, appropriate design, and awareness. [more]

- There is no commonly agreed upon set of interventions under the term of market shaping, but they can be broadly categorized by the main type of lever they use: reduce transaction costs (e.g., pooled procurement), increase market information (e.g., strategic demand forecasting), balance supplier and buyer risks (e.g., advance market commitments). [more]

- New developments have been taking place in the field in recent years: (1) New intervention types have been devised and implemented (e.g., ceiling price agreements); (2) there has been a drive toward institutionalization with the launch of several new organizations whose sole policy instrument focus is market shaping (e.g., MedAccess); (3) there is an increase in co-ownership with national governments in low- and middle-income countries (LMICs); (4) the field is increasingly experiencing diminishing returns as most of the “low-hanging fruits” have been picked, and projects are getting more complex with narrower indications and smaller health impacts. [more]

- Market shaping has recently seen both wins and disappointments. Recent wins include: (1) Results for Development’s (R4D) amoxicillin dispersible tablets (amox DT) program; (2) ceiling price agreements for optimized antiretroviral (ARV) regimens; (3) a ceiling price agreement for HIV self test; (4) significant price reductions in vaccines achieved by Gavi. Recent disappointments include: (1) the continued price instability of malaria ACTs; (2) the failure of a uterotonic agent to be registered in Kenya; (3) the sole supplier of malaria rapid diagnostic tests (mRDTs) threatening to leave the market due to unsustainably affordable prices; (4) a tuberculosis (TB) drug in Brazil not being procured. [more]

- We describe three case studies of recent market shaping activities:

- The Affordable Medicines Facility—malaria (AMFm) was launched by the Global Fund in 2009 (and discontinued in 2017) as a financing mechanism aimed at increasing access to affordable and high-quality antimalarial medicines (ACTs) in eight LMICs. It consisted of price negotiations with manufacturers, a buyer subsidy, and various supportive programmatic interventions. The program was very controversial, but is overall considered successful at achieving its goals. [more]

- Gavi has been coordinating pentavalent vaccine (a vaccine protecting against five diseases) market shaping interventions since 2001, mainly to increase uptake of the Hib and HepB vaccines in LMICs while reducing the number of shots needed. This was a large undertaking involving many actors and interventions (e.g., pooled procurement, market analyses, demand forecasts, technical assistance to regulators and manufacturers). The pentavalent vaccine is the first Gavi-supported market to reach fully satisfied demand. Moreover, pentavalent vaccine prices in 2023 are only one-third of the price level in 2006. However, the interventions may have had some unintended consequences. [more]

- Unitaid/CHAI’s Paediatric HIV/AIDS and Innovation in Paediatric Market Access (IPMA) projects ran between 2007 and 2016, largely as a way to pool and coordinate procurement for pediatric ARVs. The Paediatric HIV/AIDS project focused on pooled procurement, price negotiations with suppliers, and consolidating ARV formulations, while IPMA focused on technical assistance and global coordination efforts. Prior to 2010, Unitaid served as the sole funder and procurer. The projects were evaluated as being highly successful in terms of public health impact, near- and medium-term market effects, and cost-effectiveness; however, the transition away from central procurement in 2010 was likely inadequately executed. [more]

- Many actors are involved in the market shaping field (e.g., Global Fund, Gavi, UNICEF, USAID, R4D) and perform three functions: funding, research, and implementation. BMGF is the main philanthropic funder of market shaping work. Most actors we’ve seen focus on the “big three” infectious diseases (TB, HIV/AIDS, malaria), and/or on vaccines. [more]

- Our impression is that the mandates of most (with the exception of some more recent organizations) of the major players do not stipulate any particular market shaping approaches, but rather a focus on specific diseases, product types, and public health goals). We have not found any comprehensive overview of funding streams in the market shaping field, but some example funding figures we found point to a total annual spending in the billions of dollars. [more]

- Market shaping funders and implementers have historically neglected several

areas, which we summarize in three groups: [more]

- Therapeutic areas: Non-communicable diseases, certain infectious diseases (e.g., hepatitis), maternal and child health (excluding family planning), and cross-therapeutic products (e.g., medical oxygen) have been neglected relative to the “big three” infectious diseases (HIV/AIDS, malaria, TB). Moreover, comprehensive primary care provision has received less attention relative to verticalized, donor-supported programs.

- Intervention types: Market shaping interventions have historically focused heavily on the supply side, with less attention devoted to the demand side. Moreover, interventions focused on the scale-up of new medical products have lagged behind the support of R&D programs. Non-traditional financing solutions are under-utilized.

- Market types: National and subnational, and “fragmented” product markets have been neglected mainly due to structural challenges (e.g., the market for maternal and child health products is highly decentralized and fragmented across many different national health ministries and procurers).

- We spotlighted two intervention types:

- Pooled procurement dates back to the 1970s and means that buyers “pool” their financial, technical, or human resources to purchase products to increase the buyers’ bargaining power and procurement efficiencies. It is a frequently used intervention type to help reduce prices, improve quality standards, increase product availability, and speed up drug access. [more]

- Antibiotic subscription models are a novel concept in which payments to antibiotics manufacturers and developers are delinked from the volumes sold. They are used to increase pharmacological innovation in antibiotics while at the same time reducing incentives for antibiotic overprescription to hinder the spread of antimicrobial resistance. Two pilots are currently being implemented in the UK and in Sweden. [more]

Market shaping 101

Market shaping is a means of creating well-functioning markets by targeting the root causes of market shortcomings

Market shaping is a broad and somewhat vague term that is interpreted slightly differently across actors in the field.1,2 The broader concept of “market shaping” has over the past 20 years been studied by several academic disciplines, including marketing science,3 political economy, and global health. In this report, we focus on market shaping by the state and philanthropic actors within global health — not by firms. Moreover, we focus on health commodities and medicines.4

Market shaping is a means of creating well-functioning markets through improving specific market outcomes, such as availability and access to high quality products, by targeting the root causes of market shortcomings. According to a landmark 2014 USAID report, the end goal of market shaping in the global health field is to improve public health (Center for Accelerating Innovation and Impact [CII], 2014, p. 11).

In the context of global health, “the common denominator of market shaping interventions is a design to disrupt current practices or transform existing market structures, as opposed to adapting or conforming to them” (CII, 2014, p. 9).

Market shaping does not encompass a clearly defined set of interventions. USAID (CII, 2014, p. 29) describe 16 different interventions under the market shaping term (e.g., pooled procurement, market landscape analysis, advance market commitment), but in practice, this is not very clear-cut:

- Market shaping interventions tend to be catalytic, timebound, and have a strong focus on influencing buyer and supplier interactions. They usually go hand-in-hand with routine and ongoing programmatic interventions (e.g., healthcare provider training), but the distinction between these two categories of interventions is a continuum rather than a dichotomy.

- In practice, the labeling of interventions is not always meaningful. Different interventions can sometimes go under the same label, or new labels can be used for the same types of interventions.5

- Different organizations list different sets of interventions under the umbrella of market shaping activities. For example, CHAI distinguishes between “interventions” (e.g., clinical studies, manufacturing optimization, coordinated supply planning) and “financial tools” (e.g., payment guarantees, impact investment, product subsidies), which can be used to enhance “interventions” (CHAI, personal communication). By contrast, USAID’s list of interventions (CII, 2014) best overlaps with CHAI’s list of financial tools. USAID’s approach appears to be more mainstream to us.

Market shaping interventions can be carried out by different actors. In many cases, they are collaborations between several actors/stakeholders, such as national governments, donors, global health organizations, and regulators.

Market shaping typically addresses shortcomings in one or several market characteristics: affordability, availability, assured quality, appropriate design, and awareness

According to USAID (CII, 2014, p. 5), “a well-functioning healthcare market with public and private sector participation requires manufacturers to produce high-quality products, distributors to deliver the necessary quantities, providers to administer them correctly, and patients to be educated and active participants in their own health.”6

In practice, however, markets are often subject to various shortcomings, which can compromise public health outcomes. For example, developers may have insufficient incentive or perceive a too high risk to develop a new product, manufacturers may lack sufficient quality assurance to produce high-quality products, or products may be unaffordable or available in insufficient quantities for consumers.

There is no unified approach to investigate market shortcomings, but our impression is that most major organizations use some variation of the “five As” mnemonic7 laid out by USAID (CII, 2014), which is a framework to investigate shortcomings in each of the following five market characteristics. See the “five As” and their definitions in Table 1 below.

Table 1: The “five As” of market characteristics (CII, 2014, adapted from p. 21)

| Market characteristic | Definition |

| Affordability | Extent to which the price point maximizes market efficiency between players and suppliers to support health outcomes |

| Availability | Capacity and stability of global supply to meet demand; and consistency of local access at service delivery points |

| Assured Quality | Level of evidence that a product is consistently efficacious and safe |

| Appropriate Design | Degree to which possibilities of technology maximize cultural acceptability, choice, and ease of use |

| Awareness | Extent to which end users, healthcare providers, and key influencers can make informed choices about product use |

Shortcomings in each of those market characteristics can have different root causes. For example, products might have high prices and thus be unaffordable for consumers for various reasons, such as high supplier margins, expensive inputs, or high transaction costs (CII, 2014, p. 6). See Appendix A for an overview of sample metrics that can be used to investigate these market characteristics, and some example market shortcomings for each of the “five As.” Another approach to investigate market shortcomings is to observe failures along the product value chain, ranging from initial R&D through to service delivery/user adoption (see Figure 1 below from CII, 2014, p. 13). We provide some example market shortcomings along the product value chain in Appendix 2.

If shortcomings exist in any of these market characteristics, then it may potentially be appropriate to engage in market shaping interventions. Note, however, that an investigation of market shortcomings only provides a starting point, and further analysis is necessary to determine whether a market shaping approach is beneficial and feasible. For example, expected benefits need to be weighted against potential drawbacks and risks, and market shaping interventions need to be weighed against programmatic interventions. Moreover, various other factors and implementation constraints need to be considered, such as the political or regulatory constraints (CII, 2014, p. 28). We are not aware of any straightforward rules or heuristics by which to decide whether to engage in market shaping activities.

There is no clearly defined set of market shaping interventions, but typical examples are pooled procurement, advance market commitments, and strategic demand forecasting

Figure 1 below (from CII, 2014, p. 13) shows examples of interventions as distributed along two dimensions, the product value chain on the horizontal axis, and the market shaping/global health programmatic continuum on the vertical axis (also mentioned here). This figure is more illustrative rather than definitive or comprehensive.

Figure 1: An illustration of the market shaping/global health programmatic continuum. From “Healthy markets for global health: A market shaping primer,” by Center for Accelerating Innovation and Impact, 2014, United States Agency for International Development, p. 13 (https://perma.cc/M4RD-KTC4). In the public domain.

These interventions can also be roughly categorized by the type of lever they use (adapted from Savage et al., 2021; CII, 2014; see Figure 2 below), i.e.:

- Reduce transaction costs — Interventions that aim to reduce transaction costs by streamlining demand (e.g., by simplifying procurement) and thereby making processes more efficient, demand more predictable, and increase economies of scale

- Increase market information — Interventions that increase market information and reduce information asymmetries (e.g., through data collection/analysis or promoting existing data/analyses) and thereby facilitate coordination across different actors

- Balance supplier and buyer risks — Shifting some financial supplier risks to donors/purchasers and thereby make market engagement more attractive to suppliers (such that e.g., new suppliers enter the market)

Reducing transaction costs could, for example, involve “pooling procurement to create a more robust and consistent demand, thereby improving profitability and predictability in the market” (CII, 2014, p. 14). In practice, these levers typically overlap and interventions use one or several of them. For example, pooling procurement can also increase market information by making aggregate demand more visible.

In addition, certain interventions are more heavy-handed — and should thus be used more sparingly — than others. According to Susie Nazzaro (former BMGF), volume guarantees rank among the most heavy-handed interventions, while rotating product stockpiles and buydowns or copayments are moderately heavy-handed. By contrast, demand forecasting, procurement process improvement, procurement strategy, and global access agreements are relatively light-touch.

We created a summary table of the market shaping interventions, as defined by USAID (CII, 2014). This table summarizes information on what the different interventions are, some examples, their respective benefits and drawbacks, and other relevant links. Note that this overview is based on information that is almost a decade old, and is thus outdated in some parts. For example, we know that some new market shaping approaches have been developed since then, such as antibiotic subscription models (see next section).

To our knowledge, no other overview of the market shaping field has been published in the last decade. However, an expert pointed out to us that the Bill & Melinda Gates Foundation (BMGF) has recently commissioned a “Market Dynamics Thought Leadership” project aiming to produce a refresh of USAID CII’s (2014) market shaping primer.

Figure 2: Market shaping interventions categorized by root causes addressed. From “Healthy markets for global health: A market shaping primer,” by Center for Accelerating Innovation and Impact, 2014, United States Agency for International Development, p. 29 (https://perma.cc/M4RD-KTC4). In the public domain.

The last decade has seen new developments in the field on several fronts

Expert interviews informed this section. We learned that BMGF is currently undertaking a “Market Dynamics Thought Leadership” project aiming to produce a refresh of USAID CII’s (2014) market shaping primer; that project (due for completion in Q1/Q2 2024) will likely shed even more light on recent developments. We have not been able to get in touch with the relevant team at BMGF.

In interviews with several senior US-based market shaping experts, we learned of several recent trends and developments in the formulation and implementation of market shaping in global health.

First, in terms of intervention options, major projects are devising, scrutinizing, and implementing novel market shaping approaches,8 i.e., ones that were not included in USAID CII’s (2014) primer and have been utilized in the decade since its publication. Two examples of novel approaches emerged from our conversations with interviewees:

- Ceiling price agreements: These involve manufacturers capping the prices of medical products in LMICs and agreeing to provide a certain quantity of product. For example, in 2017, ceiling price agreements for a new dolutegravir-based ART regimen were jointly brokered with industry by multiple partners — including the governments of South Africa and Kenya, UNAIDS, BMGF, CHAI, USAID, DFID, the Global Fund, and Unitaid (UNAIDS, 2017).

- Market shaping paired with outcomes-based financing. This serves the dual purpose of ensuring access and encouraging appropriate use. An expert mentioned opportunities to investigate the possible combined use of pooled procurement and financing tools tied to outcomes. In the context of antimicrobial resistance, outcomes-based financing ties funding to antimicrobial stewardship initiatives such as increased access to diagnostics (see also our section on antibiotic subscription models).

Second, representing a drive toward institutionalization, several new organizations whose sole policy instrument focus is market shaping have launched in recent years, including MedAccess (in 2017) and SEMA Reproductive Health (in 2021). According to an expert, the increased interest by multiple organizations in utilizing and investing in market shaping approaches9 is “a testament to how this approach has become more … mainstreamed, accepted, and endorsed.”10

Third, more efforts are directed toward boosting co-ownership of market shaping strategies in LMICs that have traditionally played relatively passive roles in determining the interventions they receive, thus putting them in the “driver’s seat.”11 One expert raised the example, in the context of multiple micronutrient supplements, of BMGF co-developing a roadmap with the governments of high-burden countries in advance of considering specific interventions. Another expert gave the example of a co-creation workshop wherein the Ghana Health Service convened, with USAID and other donor support, the regional health leads of six priority regions and other country-based stakeholders to discuss health priorities and their relevance for an open call for innovation and building an innovation ecosystem; the discussion then served as the basis of a subsequent Country Innovation Platform call for proposals funded by Grand Challenges Canada (see also Grand Challenges Canada, n.d.).

Fourth, Ripin stated that many of the “big, easy deals” in market shaping — typically those made at the global level — have already been done. Ripin noted that while the cost of market shaping (including analyses, negotiations, and financing) has stayed relatively constant, the size of individual deals is often smaller.12 Potential responses to this phenomenon vary. One response is illustrated by CHAI’s and R4D’s present focus on decentralized markets at the national, subnational, and local levels, which are where most of the remainder of opportunities may lie. Another response, according to Lakhani, is to shift attention from commodities to services, whose markets are more complex and harder to de-risk.13

The recent track record of market shaping interventions includes both successes and disappointments, as well as large-scale interventions

Market shaping has seen several recent wins and disappointments

Below we catalog several notable recent wins and disappointments, by and large gleaned through expert interviews. (We consider it likely that failures or disappointments are much less publicized than successes, and that expert interviews represent the best source of information.) We advise against drawing any conclusions about the competence of organizations involved in the below initiatives based on the cataloged wins and disappointments alone.

Recent wins:

- R4D’s amox DT program: R4D’s public sector policy brief states that, in Tanzania, the proportion of facilities with amox DT rose from 47% to 61% over eight months in 2017 (R4D, 2019).

- Market shaping stakeholders also named the following as recent wins, notable

for their innovative market shaping approaches:

- An internationally jointly convened ceiling price agreement for optimized ARV (dolutegravir) regimens. We discuss this in more detail above.

- A ceiling price agreement for HIV self test. The price of the test was recently capped at $1 per test, an important step toward successfully increasing affordability and accessibility.

- While not especially recent, we learned from desk research that in 2011 Gavi reported achieving significant price reductions in three vaccines — specifically, the pentavalent (see also below), rotavirus, and HPV vaccines (Gavi, 2011a). Gavi’s press release states that the prices of rotavirus and HPV vaccines were each discounted by 67% (Gavi, 2011a), while the price of pentavalent vaccine was projected to drop by 29% from 2007 to 2011 (Gavi, 2011b).

Recent disappointments:

- Artemisinin-based combination therapies (ACTs) for malaria: Neel Lakhani (CHAI) said that the market for ACTs is “subject to significant fluctuations” owing to historical fluctuations in underlying commodity prices (e.g., artemisinin).14

- The uterotonic agent market in Kenya: An expert stated stated that an initiative to bring a new uterotonic agent to market in Kenya had successfully built demand in communities, but failed to simultaneously register the product in the FDA equivalent. According to the expert, neither the old nor the new uterotonic agent was available at some providers.

- The global malaria rapid diagnostic test (mRDT) market: According to an expert, Abbott was the only mRDT supplier globally and threatened, during the COVID-19 pandemic, to leave the mRDT market unless it could raise prices, because it found the COVID-19 rapid diagnostic test market much more profitable than the mRDT market. The dependence of the global market on a single supplier and excessively low mRDT prices (resulting from market shaping) — representing an imbalance between affordability and commercial sustainability — resulted in this situation.

- A niche TB drug in Brazil: While this is not a particularly recent example (dating back 14 years), Ripin stated that CHAI helped to negotiate lower prices and expedite regulatory filing for a niche TB drug in Brazil. CHAI typically utilizes its in-country networks to undertake supplementary demand-side interventions to support the deals and lead to substantial savings. CHAI doesn’t have a presence in Brazil and therefore didn’t do the typical work on program planning and local adoption. This may in part have led to the fact that this product wasn’t ultimately procured.

It is difficult to make causal attributions when evaluating market shaping attempts

Typically, market shaping approaches are evaluated using a before-after comparison of several types of indicators and with a mix of qualitative and quantitative metrics.15 Several factors make a causal attribution in the space difficult:

- Most organizations combine several market shaping approaches, or they combine market shaping approaches with programmatic interventions.16 Thus, in most cases, it’s not possible to evaluate the impact of individual market shaping approaches, but only the combined approach.

- There is usually no control group for comparison, as market shaping interventions affect all actors in a market.17

- Kremer et al. (2020) found that the pilot pneumococcal AMC likely sped up vaccine adoption, using the rotavirus vaccine (for which there was no AMC) as an approximate counterfactual (p. 5). We also discussed this in a previous Rethink Priorities report (Kudymowa et al., 2022).

- Dykstra et al. (2015) used a regression discontinuity design to estimate Gavi’s impact on vaccination rates and found that Gavi increased vaccination rates for some vaccines (e.g., HiB and rotavirus), but not for others. However, it is not possible to know to which extent the effect was through Gavi’s market shaping interventions vs. Gavi’s other activities.

Three case studies of recent, large market shaping interventions

In the following, we describe three case studies of recent, large market shaping interventions that we deem reasonably representative of activities in the space. We chose them mainly based on the availability of independent (third-party) evaluations or peer-reviewed scientific publications.18

Affordable Medicines Facility—malaria (AMFm)

Summary: The AMFm was a financing mechanism by the Global Fund aimed at increasing access to affordable and high-quality antimalarial medicines (ACTs) in eight LMICs. It consisted of price negotiations with manufacturers, a buyer subsidy, and various programmatic interventions. The program was controversial, but is overall considered successful at achieving its goals (albeit to varying degrees across countries).

What is the AMFm?

In 2009, the Global Fund launched the AMFm as a financing mechanism aimed at expanding access to affordable and high-quality antimalarial medicines, specifically artemisinin-based combination therapies (ACTs).

The AMFm was based on three elements (adapted from Tougher et al., 2012, p. 1918):

- Price reductions through negotiations with manufacturers of quality-assured ACTs (QAACTs)19

- A buyer subsidy, via a co-payment by the Global Fund to participating manufacturers, for purchases made by eligible public, private, and non-governmental organization importers

- Interventions to support AMFm implementation and promote appropriate antimalarial use (e.g., provider training to promote ACT use).

From 2010 to 2011, the AMFm piloted eight national level programs in seven countries in sub-Saharan Africa20 and was supported by various partner organizations and funders.21 Until 2012, $336 million was spent on drug copayments and $127 million was spent on supporting activities (ibid, p. 1918). The AMFm financed and delivered about 156 million doses of QAACT to participating countries until December 2011 (Tougher et al., 2012, p. 1918).

In 2012, the AMFm was ended as a standalone program and integrated into the Global Fund’s “core system for awarding malaria-control grants to countries” (“Too much to ask,” 2012). We have not been able to find much information about the activities and outcomes of the AMFm during this period and therefore focus our attention on the pilot phase. The AMFm was discontinued in 2017 (Rosen et al., 2020, p. 3). According to an editorial in Nature (“Too much to ask,” 2012), this decision may have been driven by “long-standing US opposition to the AMFm.”22 Tougher et al. (2021) note that it may have been due to “reductions in allocations to countries and shifting priorities.”

What problems did it aim to solve?

The AMFm was introduced to increase the uptake of recommended antimalarial drugs in sub-Saharan Africa, which was low partly due to a high cost of drugs.23 The AMFm had four main objectives (adapted from AMFm Independent Evaluation Team, 2012, p. xix):

- Increase ACT affordability

- Increase ACT availability

- Increase ACT use, including among vulnerable groups

- “Crowd out” oral artemisinin monotherapies, chloroquine and sulfadoxine-pyrimethamine (SP) by increasing the market share for ACTs.

What were the outcomes?

The Global Fund commissioned an independent evaluation of the AMFm to assess whether its four objectives had been achieved in the pilot program (AMFm Independent Evaluation Team, 2012). The evaluation was based on a before-after comparison24 covering all participating countries.25 There was no control group, so the results need to be interpreted with caution.26 Our impression is that the pilot programs have generally been considered a success by the group of independent evaluators, though the level of success varied across the eight project areas.

Some key findings were:

Briefly, the benchmark of a 20% point increase in QAACT availability was met in five out of the eight pilots. The benchmark of a 10% point increase in QAACT market share was met in four pilots, with a further three having weak statistical evidence. Finally, the benchmark of QAACT prices falling below three times the price of the most popular non-ACT anti- malarial in the country was met in five pilots. When applied to the private sector alone, the independent evaluation’s conclusions regarding the success metrics still hold. Positive market shifts were found to be largely due to changes in the private for-profit sectors in pilot countries; indeed, the subsidy facility was described as a ‘game changer’ in the private for-profit sectors of all but two countries by the independent evaluators. A systematic review of the literature examining the effects of anti-malarial subsidies likewise found subsidies to be successful in increasing availability and reducing costs of ACT. Furthermore, improved availability and affordability tended to be equitable between rural and urban areas, and across income gradients. (ACTwatch Group et al., 2017, p. 3, emphasis ours; see AMFm Independent Evaluation Team, 2012, p. xxiii, for more detail)

See AMFm Independent Evaluation Team (2012, p. xxii) for an overview of potential success and hindering factors of the AMFm according to AMFm IE (2012).

Overall, the program was controversial. Some were pessimistic about it, for example due to “concern that the subsidies would be captured by intermediaries and not passed on to consumers, that monotherapies would continue to dominate market share because of their familiarity and perceived effectiveness, and that the poorest would not benefit because drugs are not free” (Tougher et al., 2012, p. 1917). Moreover, Oxfam criticized the AMFm for increasing the possibility of misdiagnosis and overtreatment with ACTs (Lieberman, 2012).27

On the other hand, many commentators considered it a success and advocated for a continuation of the program. A Nature editorial opined that “whatever its detractors might say, the programme has succeeded in getting effective antimalarials to the only places in rural areas where most parents can get treatment for a child whose life is threatened by malaria,” stating also that “the AMFm’s critics also note that [...] selling ACTs over the counter inevitably leads to overtreatment [...]. But overtreatment has long plagued all malaria-control programmes, and would happen with or without the AMFm” (“Too much to ask,” 2012). Moreover, according to Talisuna et al. (2012), “AMFm has worked where nothing else does, and even at scale, it should be affordable globally if malaria continues to be prioritized. [...] But the basic architecture of the AMFm subsidy and price negotiations should continue and expand.” According to an op-ed by Nobel laureate and economist Kenneth Arrow (2012), “this initiative is an interim measure to ensure that fewer children die for lack of effective anti-malarials. [...] The risk is that efforts to develop and implement ‘the perfect’ will end up killing ‘the good’ in the process.”

Gavi’s pentavalent vaccine market shaping interventions

Summary: Gavi has been coordinating pentavalent vaccine market shaping interventions to increase uptake of the Hib and HepB vaccines in LMICs in a large undertaking, involving many actors and interventions (e.g., pooled procurement, market analyses, demand forecasts, technical assistance to regulators and manufacturers). The interventions can be considered a success as the pentavalent vaccine has reached fully satisfied demand. However, there may have been some unintended consequences.

What is Gavi’s pentavalent vaccine support?

The pentavalent vaccine is a five-in-one vaccine that protects against five diseases, including diphtheria, tetanus, pertussis (whooping cough), hepatitis B vaccine (HepB) and Haemophilus influenzae type b (Hib). Gavi started offering the pentavalent vaccine to countries in 2001 to increase the low uptake of Hib and HepB vaccines by including them in routine immunization programs in LMICs, while reducing the number of shots needed (Gavi, n.d.-b).

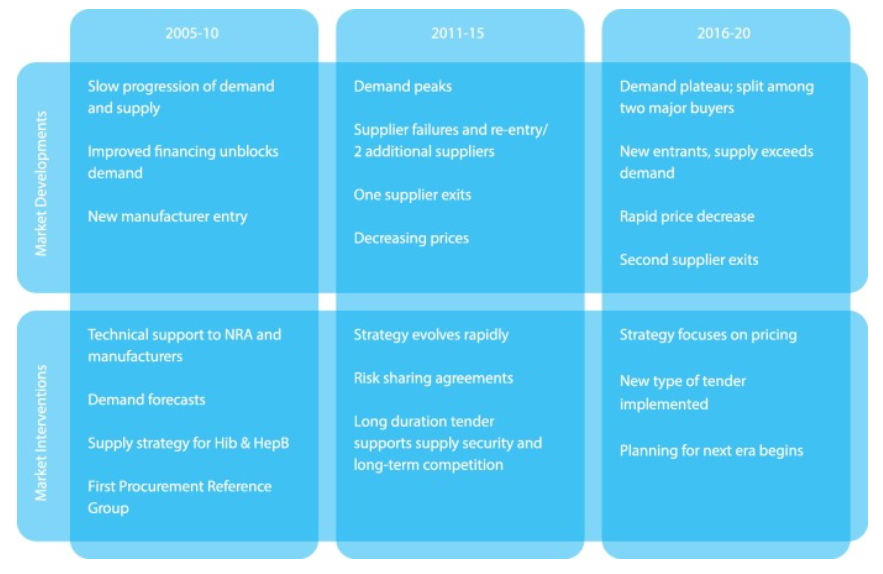

Gavi’s pentavalent vaccine support can be broadly divided into three phases (see also Appendix C for a graphical overview of these phases):

- 2001-2010: Demand generation

Gavi’s initial approach was to increase the availability and affordability of vaccines by “providing funding, generating and organizing demand from countries, and using centralised procurement to increase market influence” (Malhame et al., 2019, p. 2). These interventions were later complemented by demand forecasts by the Gavi Secretariat, publication of price data by UNICEF, and technical assistance for National Regulatory Authorities (NRAs) and vaccine manufacturers provided by the WHO (Malhame et al., 2019, p. 5).

During this phase, demand increased relatively slowly but steadily.28 Prices per dose dropped from $3.60 in 2005 to $3.20-2.25 in 2010. Moreover, four new manufacturers of pre-qualified vaccines entered the market, but then supply became more volatile as one vaccine lost its pre-qualification status (Malhame et al., 2019, p. 5). A 2008 evaluation found that while demand generation had been successful, there were still deficiencies at the supply side, such as a low supply stability and affordability of the pentavalent vaccine relative to Gavi’s initial goals (Malhame et al., 2019, p. 2).

- 2011-2015: Supply generation and

decreasing prices

In 2011, Gavi revised its Supply and Procurement Strategy by prioritizing supply, costs, and innovation, supported by increases in information and transparency. A volume guarantee was introduced by UNICEF. WHO continued to provide technical assistance to NRAs and manufacturers and was accompanied by additional technical assistance to manufacturers by PATH (and funded by BMGF) to increase production efficiencies. UNICEF started closely monitoring vaccine availability, published market and price analyses, and hosted consultations with manufacturers. It also introduced long-duration tenders to ensure supply security and long-term competition BMGF introduced a risk-sharing agreement in 2012 that aimed to increase supply. Gavi created the Healthy Market Framework in 2015 that helps market shaping partners assess the trade-offs between different market attributes and priorities (Malhame et al., 2019, pp. 2-5).

Supply increased rapidly, with two new manufacturers in India and Korea entering the pentavalent vaccine market. By 2015, seven prequalified vaccines were on the market, and prices had reduced further to $2.35-1.19 per vaccine dose. Demand from Gavi-supported countries reached ~250 million doses in 2015. In 2015, India (whose volume represents one-third of the global total pentavalent vaccine market), started procuring the pentavalent vaccine independently and became the second major buyer (Malhame et al., 2019, pp. 2-5).

- 2016-2020: Longer-term view of

markets

Gavi revised its Supply and Procurement Strategy again for the 2016-2020 period, to take a more long-term view of markets that included “identifying the point when a market no longer requires market shaping interventions, monitoring unintended consequences of market shaping activities, and to improve support for product innovation”. Risk-sharing interventions ended and risk-taking was shifted to manufacturers. More countries (besides India) started to self-fund procurement. By 2016, demand reached a plateau and supply capacity was reliable and exceeded demand. Prices per dose dropped further to $1.20-$0.69 per dose until 2016 (Malhame et al., 2019, pp. 2-7).

In total, Gavi spent $3.5 billion on pentavalent vaccine procurement from 2001 to 2018, which was channeled mainly through UNICEF, the PAHO Revolving Fund (Malhame et al., 2019, p. 2).

What problems did it aim to solve?

In the early 2000s, vaccine coverage for the HepB and the Hib vaccines were very low in LICs,29 and was likely related to a “lack of disease burden awareness, financial constraints and the poor suitability of these vaccines for lower-income countries” (Malhame et al., 2019, p. 2). Some of the goals of Gavi’s pentavalent vaccine support were (adapted from Gavi, n.d.-b):

- Boost uptake of high-quality Hib and HepB vaccines via increased availability and reduced prices

- Cost savings by combining five different vaccines in a single vial (e.g., savings in terms of equipment, delivery, and disposal) and less environmental impact

- Increasing convenience of vaccination by reducing the number of injections needed

What were the outcomes?

Our overall impression of the market shaping activities related to the pentavalent vaccine coordinated by Gavi is that they were a success, though it is possible that we missed some critical voices and controversies in the literature. Moreover, we would like to emphasize that while various outcomes have been reported and attributed to Gavi’s support, these results cannot be interpreted causally due to a lack of counterfactual and many different interventions by a large number of actors occurring simultaneously.

According to Malhame et al. (2019), “Pentavalent is the first Gavi-supported market to reach fully satisfied demand” (p. 4). The price of a pentavalent vaccine has dropped from ~$3.6 in 2006 to $1.29-$0.78 in 2023 (UNICEF, 2022). According to Gavi estimates, their support had led to more than 661 million children being immunized with the pentavalent vaccine by 2021 (Gavi, 2023). Ozawa et al. (2017) estimated that the Hib and HepB components alone could avert 10 million deaths and 390 million DALYs, and generate more than $250 billion in economic and social value in 73 Gavi-supported countries from 2001 to 2020.

Malhame et al. (2019) concluded that “outcomes in the pentavalent market provide strong evidence of the benefits of market shaping including an ability to vaccinate nearly 80 M infants in lower-income countries per year against five diseases at a vaccine cost of ~US$2.50 per child. Supply is sourced from a diversified base of manufacturers with relatively low technical risk and vaccines satisfy customer needs. Donors and countries save >US$500 M annually when procuring pentavalent when compared with 2010 prices. Broader success of Gavi’s market shaping strategy is supported by results showing that in 2017, eight vaccine markets had supply sufficient to meet demand, against the goal of 11 vaccine markets with sufficient supply by 2020” (p. 4).

The authors also mentioned unintended consequences of these market shaping efforts, such as “altering manufacturer investments in new products or ceasing production of existing products and the potential for negative pricing consequences for other vaccines or countries. While the pentavalent results are beneficial for countries and donors, prices of ∼US$2.50 per course (∼US$0.85 per dose) raise concerns among all stakeholders about the financial sustainability of pentavalent manufacturing and supply, potentially constraining investment in next generation vaccines.”

Unitaid/CHAI’s Paediatric HIV/AIDS and Innovation in Paediatric Market Access (IPMA) projects

Summary: Unitaid/CHAI’s Paediatric HIV/AIDS and IPMA projects were implemented largely to increase access to pediatric ARVs. The Paediatric HIV/AIDS project focused on pooled procurement, price negotiations with suppliers, and consolidating ARV formulations, while IPMA focused on technical assistance and global coordination efforts. The projects were evaluated as being highly successful in terms of public health impact, near- and medium-term market effects, and cost-effectiveness; however, the transition away from central procurement in 2010 was likely inadequately executed.

What are the Paediatric HIV/AIDS and IPMA projects?

The Paediatric HIV/AIDS project, also known as the “Unitaid/CHAI Paediatric Project,” and Innovation in Paediatric Market Access (IPMA) were two complementary initiatives funded by Unitaid and implemented by CHAI between 2007 and 2016. They were intended as catalytic interventions (Global Fund, 2016) to address market failures that had led to a lack of affordable treatments for children living with HIV (CLHIV) in LMICs (Cambridge Economic Policy Associates [CEPA], 2018, pp. i-viii).

The Paediatric HIV/AIDS project was launched in 2006 following a 2005 UNICEF and UNAIDS call to action (UNICEF & UNAIDS, 2005) and ran until 2015 (CEPA, 2018, p. 5). IPMA was carried out between 2014 and 2016 after Unitaid recognized a need for further global coordination efforts (CEPA, 2018, p. 5).30 See also Figure B in CEPA (2018, p. viii), for a rough timeline of the projects.

The two projects covered the majority of the countries with the highest CLHIV prevalence, prioritizing LICs with health ministries that were most willing to engage with the program and — for the later IPMA project — those that had not yet transitioned to independent procurement (CEPA, 2018, pp. 9, 78). Total disbursements for the Paediatric HIV/AIDS project amounted to $359 million31 (CEPA, 2018, p. 5), while those for IPMA amounted to $10M (Unitaid, n.d.-a).

The projects’ key activities/interventions included (mostly adapted from CEPA, 2018, pp. 10-31):

- Pooled procurement of ARVs (Paediatric

HIV/AIDS): The project aimed to consolidate small orders of disparate regimens

by individual health ministries into larger batches, and thereby increase

supplier interest and lower prices and delivery times. CHAI oversaw the annual

selection of suppliers; this involved extensive price negotiations, both during

the initial price determination (following a “cost-plus” approach;32 see also “Cost-Plus Pricing,” 2023), and efforts to

enlist additional suppliers after a primary supplier was chosen. CHAI signed

master supply agreements with suppliers to confirm procurement. From 2010

onward, CHAI also factored in non-price criteria, favoring suppliers registered

nationally in project countries and those that demonstrated superior delivery

track records.

- From 2008 to 2010, ARVs were procured in a centralized manner through Unitaid (CEPA, 2018, p. 8). Centralized procurement was then halted “as a necessary step to ‘normalising’ the market” (CEPA, 2018, p. 8).

- In 2011, the Paediatric ARV Procurement Working Group (PAPWG), supported by CHAI, took over responsibilities for coordinating procurement; IPMA was later launched to strengthen coordination.

- Consolidation of ARV products (Paediatric HIV/AIDS): CHAI reduced the number of unique formulations procured by countries in order to improve the efficacy of pooled procurement efforts and promote better adherence to the Inter-Agency Task Team’s (IATT’s) optimal formulary list (see IATT, 2016).

- Technical assistance (Paediatric HIV/AIDS and IPMA): CHAI assisted countries with procurement and supply chain management, management of scale-up of diagnostics and treatments, adoption of international best practices in treatment and formulary, and obtaining funding for pediatric commodities.

- Global coordination efforts (IPMA): CHAI established itself as the coordinator of multiple inter-agency partnerships33 and a supplier of market intelligence. In its latter capacity it produced annual ARV market reports (e.g., CHAI, 2015) and retrospective progress reviews for PAPWG (e.g., PAPWG, 2015).

There were more than 2.6 million CLHIV in 2006 (CEPA, 2018, p. 4). Due to market failures, the supply of pediatric ARVs was particularly unreliable and prone to stock-outs (Global Fund, 2016, p. 1), contributing to extremely poor treatment rates for CLHIV (one in 15 CLHIV received ARV treatment, compared with one in five for adults with HIV; CEPA, 2018, p. 4).

High prices and low availability of pediatric ARVs prior to 2007 could be partly attributed to the high fragmented nature of ARV procurement in two respects: (1) multiple countries were ordering ARVs separately, sporadically, and in small quantities (CEPA, 2018, p. 7); (2) countries were ordering a large number of ARV products with “largely duplicative formulations and doses” (Global Fund, 2016, p. 1).

What were the outcomes?

Our impression is that the Unitaid/CHAI Paediatric HIV/AIDS project — and to a lesser extent IPMA — was extremely successful in terms of its public health impact and cost-effectiveness. However, the way in which the Paediatric HIV/AIDS project’s transition away from centralized procurement was handled received mixed evaluations from partners. The projects also seem to have been largely successful in terms of its near- and medium-term market outcomes, but the pediatric ARV market’s long-term sustainability is still uncertain.

An end-of-project evaluation commissioned by Unitaid estimates that 160k deaths were averted (representing 9.8M YLLs) over the period 2007-2014 as a direct result of the Paediatric HIV/AIDS project and a further 61k deaths were averted (representing 1.2M YLLs) as an indirect result of treatment scale-up over the period 2014-2016, from the Paediatric HIV/AIDS project and IPMA — in total 210k deaths averted and 10.3M YLLs gained (CEPA, 2018, p. 37). The evaluation further concludes that the projects “undoubtedly delivered value for money,” estimating that USD 11 in benefits (from mortality reduction) and USD 2.22 in cost savings were realized for each USD 1 invested (CEPA, 2018, p. 49).

The transition away from centralized procurement starting in 2010 was considered by some to be “the most fundamental challenge” facing the project (CEPA, 2018, p. 51), and has been criticized for inadequate planning and consultation with countries and partners. According to the evaluation, project consultees drew unfavorable comparisons about the ease of transition with other Unitaid/CHAI projects.

According to the evaluation, “The Paediatric HIV/AIDS project was essential for catalysing and strengthening the market for ARV treatment for children” (CEPA, 2018, p. 46), citing price reductions of between 35% and 81% and the creation and consolidation of pediatric formulations. However, the evaluation states that long-term market sustainability remains uncertain, with manufacturers finding it difficult to adapt to evolving treatment standards and to “justify investments in new paediatric ARVs on a commercial basis” given the success of prevention of mother to child transmission efforts (CEPA, 2018, pp. 52-53).

Many actors are involved in funding, researching, and implementing market shaping interventions

We created a landscape table to provide an overview of the major actors in the market shaping field. The main actors encompass philanthropic foundations, government aid agencies, global health organizations, academic institutes, and strategy consulting organizations, and variously perform three functions: funding, research, and implementation.

We find that the majority of interventions are carried out through partnerships among multiple actors, in concert with LMIC governments (both national and subnational) and industry partners. For example, the Global Fund (n.d.) reports working with Unitaid, CHAI, USAID, among other groups. In our conversation, An expert said that, within philanthropy, BMGF is the main funder of market shaping work, and that BMGF works with three partners in research/strategy and implementation: R4D, CHAI, and PATH.

Most of the groups and interventions we’ve seen choose, or have a mandate (see below), to focus on a relatively small set of diseases and product types, including malaria, TB, HIV/AIDS, and vaccines. A smaller number of groups, including Norad, are involved with market shaping related to NCDs (Kruse & Beattie, 2022).

We also have the impression that pooled procurement is one of the most common approaches, and potentially the approach that receives the largest amount of funding (see, e.g., here where we provide some example funding streams, showing that pooled procurement activities can be in the billions USD).

Most major funders and implementers focus on specific diseases or product types rather than specific market shaping interventions

Our tentative impression is that the mandates of most (with the exception of some more recent organizations) of the major players do not stipulate any particular market shaping approaches, but rather a focus on specific diseases, product types, and public health goals.

We skimmed the missions and strategies of several of the major players. Several of them have specific market shaping strategies (e.g., Gavi, n.d.-a, Global Fund, 2015), while others mention market shaping as part of their overall strategies (e.g., Unitaid, 2022). Most of the strategic documents we have reviewed do not mention any specific market shaping approaches, but rather focus on public health goals & specific diseases or product types. The Global Fund (2015) strategy is one exception where specific market shaping tools are stated.34 The public health goals related to market shaping strategies are fairly similar across organizations and usually focus on investigating and tackling market shortcomings related to some combination of the following market characteristics: affordability, availability, assured quality, appropriate design, and awareness.

We are aware of two recently founded organizations in the field that explicitly aim to improve health markets and tackle market inefficiencies as part of their mandate. MedAccess and SEMA Reproductive Health are the only two organizations we are aware of whose sole policy instrument focus is market shaping.

David Ripin and Neel Lahkani mentioned that some global procurement agencies have procurement/governance stipulations that constrain the types of interventions they can implement. For example, some organizations are, by their mandates, not allowed to use certain financial instruments, (e.g., make multi-year commitments, or concessionary loans). In such cases, it can be beneficial for these organizations to cooperate with intermediary organizations (e.g., financing organizations like MedAccess) that are able to execute these types of transactions.

No comprehensive overview of funding streams exists, but example figures point to a total annual spending in the billions of dollars

We found little information on funding streams related to market shaping interventions. To our best knowledge, no comprehensive overview of funding streams in this field exists, and we would be surprised if there was one.35 Moreover, the organizations we have looked at did not mention any or only a small subset of their market shaping activities in their financial reports/statements.36 In most cases, organizations report their spending by disease or country, but not by market shaping activities. According to an interviewee, BMGF is the primary donor related to market shaping activities.37

Some noteworthy example funding figures we found:

- A Dalberg (2014) overview of market shaping efforts in the family planning sector found >20 initiatives representing >$450M in donor funding (p. 11)

- Unitaid invested a total of $157M (Unitaid, n.d.-d) in the quality assurance of health products (particularly the WHO Prequalification services; Unitaid, n.d.-e) and $2.8M (Unitaid, n.d.-b) in market analysis (particularly ACTwatch; Unitaid, n.d.-c).

- In 2021, the Global Fund dedicated about 1/3 (~$1.7B) of its grant expenditure to its Pooled Procurement Mechanism38 (Global Fund, 2021, p. 48).

- The “Gavi COVAX AMC began with a seed funding of US$ 505 million. [...] A target was set to mobilize US$2 billion by the end of 2020 [...]” (Gavi, 2022, pp. 15-16).

- In 2015, UNICEF procured ~$1.3 billion worth of vaccines.39

As finding comprehensive information on funding streams in the market shaping field proved to be a non-trivial and likely very time-consuming40 task, we decided to deprioritize it in agreement with GiveWell.41

Several therapeutic areas, intervention types, and market types have historically been neglected in market shaping

Market shaping funders and implementers have historically neglected several areas. We classify these gaps as falling into three groups: therapeutic area, intervention type, and market type:

Gaps in therapeutic area

In our rough overview of the market shaping landscape, we found very few market shaping interventions for non-communicable diseases (NCDs) in LMICs, even though drugs and other commodities for those diseases are, at least in some cases, also subject to problems related to accessibility, quality, etc.42 We suspect that this might be attributable to three reasons: the higher relative burden of communicable diseases in LMICs, board-defined mandates (e.g., that of the Global Fund), and structural challenges. Interviewees also highlighted that global health market shaping has not focused on NCD commodities and noted that the current scope of many global health actors does not include NCDs. They further noted that NCDs suffer from similar structural challenges (i.e., decentralized funding and procurement) to those we highlight below; Two experts echoed this point in our respective conversations.

Ripin further noted that certain infectious diseases, including hepatitis, have been relatively less prioritized compared to the “big three” infectious diseases of TB, malaria, and HIV/AIDS.

One expert said that market shaping solutions to the maternal, newborn, and child health (MNCH) commodity space (excluding family planning) have been difficult to design largely due to structural challenges. They explained that MNCH commodity procurers are highly decentralized, being dispersed across different national health ministries, and that it is consequently difficult to aggregate their purchasing power to a degree that is convincing for manufacturers.43

An expert stated that market shaping has historically neglected product areas that cross therapeutic boundaries, including medical oxygen (although COVID-19 has brought more attention to oxygen). They pointed to the “structure” of philanthropy as a root cause of this neglect — donors have tended to look at individual therapeutic areas, meaning products that do not necessarily count as part of a single area often “fall through the cracks” — and stated that USAID is the only major funder of cross-therapeutic area products.

Ripin pointed out that comprehensive primary care provision has received less focus than verticalized, donor-supported programs, although COVID-19 has increased attention to market access of basic commodities including blood chemistry tests, first-line antibiotics, and other primary health commodities.

Gaps in intervention type

At least until 2014, market shaping interventions tended to focus predominantly on the supply side; demand-side interventions were therefore neglected.44 This phenomenon was criticized in a 2014 CGD-hosted panel discussion on market shaping (CGD, 2014). As an example, Kanika Bahl, one of the panel discussants, explained that a heavy focus on the supply side led to a partial failure of market shaping interventions related to pediatric ARV drugs led by CHAI, as drug uptake remained low despite increased availability and accessibility of the drugs.

We are not certain about the extent to which this heavy focus on the supply side remains problematic. Our conversation with an expert suggested that an imbalance between four different market components, Supply, Demand, Regulatory, and Financing,45 could still be a concern. The expert indicated that market shapers need to do better at simultaneously addressing (“harmonizing”) multiple inefficiencies; funders and implementers have pursued siloed approaches — e.g., focusing on supply but not simultaneously pushing on the regulatory front — leading to oversights such as failing to register a new uterotonic product in Kenya, such that neither the old nor the new version was available.

Moreover, some groups could be excessively focused on reaching “discrete,” high-level milestones and inadequately address complex, on-the-ground challenges. In our conversation, David Ripin cautioned against viewing the successful negotiation or brokering of agreements as the end product of market shaping; in fact, agreements alone do not deliver affordability and access to end users unless a complex array of local-market factors, such as regulations and agreements with individual suppliers and distributors, are simultaneously addressed.

According to experts, the scale-up of new medical products has lagged behind the rate of R&D, leading to disparities in product availability between HICs and LMICs. An expert raised the example of a NASG device for postpartum hemorrhaging that was introduced in HICs but not in LMICs. Another expert noted that a potential culprit for this phenomenon is many donors’ and developers’ mistaken expectation that products will make it to LMIC markets automatically once a technology is demonstrated. Donors’ and developers’ lack of market understanding thus results in an unnecessary delay in the commencement of market shaping activities and hence in access.

An expert also singled out non-traditional financing solutions46 as under-utilized tools while mentioning that CII is increasing its overall efforts to “elevate the role that non-traditional investors can play in global health.” They particularly noted recent reports from CII that expanded on this idea, such as the blended finance roadmap (CII, 2022a) and “Unleashing Private Capital for Global Health Innovation” (CII, 2022b).

Gaps in market type

Multiple experts noted that the market shaping field has seen major successes in health areas for which large, global, centralized procurers and funders exist, such as malaria and HIV/AIDS; this can be attributed to donors’ preference for verticalized programs. However, according to one expert, a “lack of interest and attention” from donors has led to the neglect of national and subnational, or “fragmented,”47 product markets (see above for the example of MNCH commodities). The same expert expressed their concern that the present model — considering individual products at a global level — “does not lead to greater efficiency,” compared with the alternative of considering portfolios of products at a national/subnational level.

Spotlight on pooled procurement and subscription models

As we did not have sufficient time to review all market shaping approaches in depth during our work on this report, we spotlight two different approaches: pooled procurement and antibiotic subscription models.

We decided to focus on pooled procurement for several reasons: (1) it seems to be a fairly common market shaping approach; (2) there is a comparatively large evidence base relative to other market shaping approaches; (3) it can be considered a typical48 market shaping approach. We decided to also focus on antibiotic subscription models, as it is a quite novel concept which is currently gaining popularity, also within the effective altruism space,49 and being piloted in two countries. It has not been covered in the USAID CII (2014) market shaping primer.

Pooled procurement

What is pooled procurement and what problems does it solve?

What is it?

Pooled procurement50 is “a formal arrangement where financial and other resources are combined across different purchasing authorities, to create a single entity for procuring health products on behalf of individual purchasing authorities” (WHO, 2021). Essentially, pooled procurement means that buyers “pool” their financial, technical or human resources to purchase products. The basic idea is that it can increase the buyers’ bargaining power by aggregating their demand, and increase efficiencies through sharing of human resources and technical capacity (Parmaksiz et al., 2022, p. 2).

The concept dates back to the late 1970s when the the World Health Assembly endorsed pooled procurement as a means to reduce costs of pharmaceutical products,51 and became popular in the “era of global health organizations” in the late 1990s when organizations such as Gavi, PEPFAR, and the Global Fund used pooled procurement principles to provide “access to affordable and quality medicines” (Parmaksiz et al., 2022, p. 2).

What problems does it solve?

Pooled procurement is used to address various market shortcomings, such as:52

- Small market size of the buyer

- Limited technical capacity and human resources

- Insufficient incentives to manufacture or supply specific medicines or vaccines

- Low-volume high-price products (e.g., for rare diseases)

It can be used to achieve a number of different goals, such as:53

- Price reductions induced by demand aggregation (e.g., due to volume discounts or by increasing bargaining power of buyers).

- Improvement of procurement efficiency and quality standards by sharing technical capacity and human resources

- Increasing availability and securing supply sustainability by incentivizing suppliers and as a result increasing supplier competition

- Speeding up access to drugs (e.g., by facilitating the drug registration and approval process)

How is it implemented?

Several pooled procurement models exist that differ in terms of their degree of coordination. For example, “informed buying” through sharing of price and supplier information is on the low end of coordination, while “central contracting + purchasing” through a centralized procurement body is on the higher end (Nemzoff et al., 2019, p. 3).

Pooled procurement can take place within a country or across countries. Moreover, there are various possible organizational arrangements. For example, it can take place through a (cross-country) collaboration agreement,54 a third-party group purchasing organization (GPO),55,56 or a fully integrated supply chain operation (FISCO), which combines procurement with supply-chain related activities.57,58

Our impression is that pooled procurement models are typically implemented in combination with other market shaping approaches, such as demand forecasting.59

When is it suitable?

Pooled procurement requires the existence of a market with several features, such as “(i) large enough volumes; (ii) a supplier that can supply such volumes, and (iii) a buyer that commits to purchasing those volumes. For (ii) and (iii) to work, it is critical for there to be trust between buyers and suppliers” (Nemzoff et al., 2019, p. 6).

If the primary goal is to reduce prices, then pooled procurement is less suitable if there is a high level of market concentration (i.e. a low level of supplier competition), as the suppliers’ monopoly/oligopoly power “can at least partially offset the negotiating power of a pooled buyer” (Nemzoff et al., 2019, p. 22).

How commonly is it used?

Pooled procurement mechanisms are fairly commonly used in various settings and modalities. In terms of third-party GPO, the PAHO Revolving Fund and the Gulf Cooperation Council Purchasing Programme, both established in the late 1970s, were among the first cross-country pooled procurement mechanisms. They were followed by several other large global health organizations around the 1990s and 2000s, such as the UNICEF Vaccine Independence Initiative, the Global Fund, the Global Drug Facility, PEPFAR, and Gavi.60 During the COVID-19 pandemic, they have also been used in various countries and globally through the Covax initiative to procure vaccines and protective equipment (Parmaksiz et al., 2022, p. 2).

Pooled procurement has also been commonly used at the national and subnational level. Some prominent examples include centralized procurement systems for public hospitals in Denmark and Norway, and national programs (e.g., for TB, malaria, and HIV/AIDS) in India (see WHO, 2020a, p. 32).

Successes and failures

The best systematic review we’ve seen on the outcomes and reasons for success or failure of pooled procurement of medicines and vaccines was done by Parmaksiz et al. (2022). We have not reviewed the quality of the underlying studies, but we suspect that the evidence is predominantly based on case studies where a causal attribution is difficult or impossible. Moreover, as the authors explain, the literature on pooled procurement is likely biased towards successful mechanisms and favorable outcomes.61 Few studies report negative outcomes.62

Successes:

Parmaksiz et al. (2022) found that studies that investigated pooled procurement predominantly reported outcomes related to prices, availability, quality, and procurement efficiency. In the following, we summarize their findings for each of those categories:

- Prices of medicines or vaccines:

- Parmaksiz et al. (2022) found that the majority of 29 empirical studies observed a price reduction after pooled procurement was introduced. For example, Dubois et al. (2021) reviewed data from seven LMICS on various essential drugs from 16 therapeutic areas and found price reductions of 15% on average. Dubois et al. (2021) found that the price reduction was lower in markets with less supply-side competition, whereas several other studies did not find such a relationship (e.g., Singh et al., 2013). Some studies found no, or only small price reductions, or hypothesized that the price reductions might have been influenced by other factors (e.g., overall price trends in the market) (e.g., Singh et al., 2013).

- Availability of medicines of vaccines:

- Parmaksiz et al. (2022) found 11 studies that reported on the effects on medicine or vaccine availability. For example, after the introduction of the Global Fund’s Voluntary Pooled Procurement, an increased availability of malaria commodities was found (Wafula et al., 2013). Moreover, Roy Chaudhury et al. (2005) found that essential medicines in tertiary hospitals in Delhi became more available after pooled procurement. Parmaksiz et al. (2022) also mention one study that found no increase in the availability of essential medicines in primary healthcare facilities after pooled procurement was introduced in two Chinese provinces (Song et al., 2018).

- Procurement efficiency:

- Several studies pointed out that pooled procurement might be more beneficial for smaller buyers as they would, at least theoretically, benefit most from an increased bargaining power and price discounts on large orders. However, our impression is that this is more of a theoretical/hypothetical observation rather than an empirical one. Several studies found an increase in process standardizations across various pooled procurement interventions, e.g., the PAHO Revolving Fund, the Gulf Cooperation Council (DeRoeck et al., 2006), the Global Drug Facility (Kumaresan et al., 2004), as well (sub-) national programs in, e.g., Costa Rica and Australia (Budgett et al., 2017).

- Quality of products:

- Parmaksiz et al. (2022) found two papers that reported on a pooled procurement mechanism in Delhi, India that was combined with various quality-assurance mechanisms (e.g., prequalification of suppliers, inspections, testing). This set of interventions was associated with a decrease of medicines that failed quality control63 (Roy, 2013; Roy Chaudhury et al., 2005). Moreover, a study in China (Zhuang et al., 2019) found that an increase in vaccine prices after the introduction of pooled procurement may have been partly driven by an increase in quality standards, though our impression is that this is rather speculation rather than a direct empirical finding.

Parmaksiz et al. (2022) found several success factors for pooled procurement mechanisms in their systematic review of 44 studies (pp. 8-11):

- Sufficient level of technical and financial capacity both on the buyer and procurement organization side (technical capacity, e.g., to carry out demand forecasting; financial capacity to produce products)

- Compatible laws and regulations on the buyer’s side

- Independent operations of the procurement organization (e.g., to limit the potential for conflicts of interest)

- Sufficient incentives for suppliers (e.g., sufficient market size and prompt payment mechanism).

Failures:

According to Parmaksiz et al. (2022), “[v]arious pooled procurement initiatives have failed even before being realized, such as the Pacific Island Countries;64 have remained in the realization phase, such as the East African Community;65 or have failed after early operationalization, such as the Asthma Drug Facility66 or the African Association of Central Medical Stores for Essential Drugs (ACAME).”67 As we explain in more detail below, these pooled procurement interventions failed (or never occurred) for various reasons, such as funding difficulties, an unfavorable cost/benefit ratio, a lack of political will, inference with national sovereignty, prioritization of other issues, and regulatory obstacles.

We reviewed the reasons for these failures68 in more detail:

- Pacific Island Countries (Mendoza, 2010):

- The potential of exploring pooled procurement of medicines has been discussed among the Pacific Island countries since the 1990s and considered advantageous, for example, because the demand volume of individual countries is very small and would benefit from aggregation. Nonetheless, in a 2009 ministers’ meeting of Pacific Island Countries, political leaders dismissed the idea due to several concerns, such as: (1) pooled procurement may interfere with national sovereignty and potentially exacerbate existing political tensions,69 (2) aggregate demand in the region may be insufficient to result in price reductions due to economies of scale,70 (3) the costs might outweigh the benefits due to high shipping costs, large additional (advance) funding requirements for administration and operations,71 and high management costs of restructuring existing processes.72

- East African Community (Syam, 2014):

- The potential of implementing pooled procurement for antiretroviral drugs has been discussed in the East African Community since 2007. Various analyses have been conducted until a proposal for establishing a regional pooled bulk procurement mechanism has been approved by the Council of Ministers in 2008. However, there has been very little, if any, progress ever since, and it is mostly unclear why this is (with the exception that other issues like medicine registration harmonization have been prioritized relative to pooled procurement).73

- Asthma Drug Facility (Bissell et al., 2016):

- The Asthma Drug Facility has been run until 2014 when it was discontinued due to “funding difficulties and lack of demand from countries” (p. 722). We have not been able to find more detailed information on the reasons for failure.

- African Association of Central Medical Stores for Essential

Drugs (Regional Office for

South-East Asia, 2014):

- The ACAME pooled procurement mechanism was established in 1996 and successfully procured five antimicrobials at lower prices. However, no further pooled procurement was done afterwards. An analysis by Botswana’s Ministry of Health and Wellness (2021) identified several bottlenecks that the ACAME pooled procurement mechanism faced, such as, (1) a lack of harmonized medicines regulation policies; (2) limited resources allocated to joint purchasing by members (3) differences in economic status of member states; (4) lack of an institutional home for the mechanism, and (5) competition from global pooled procurement mechanisms (p. 17).

Antibiotic subscription models

What are antibiotic subscription models and what problems do they solve?

What is it?

In the context of antibiotics, subscription models refer to “fixed annual payments or minimum revenues for a set period in return for sufficient antimicrobial product supply guarantee, delinked from the volumes sold” (Boluarte & Schulze, 2022, p. 13).74 Thus, purchasers pay a fixed annual fee for a product, regardless of the numbers of product units that are needed. Our impression is that the concept is quite novel and has only recently been proposed and theoretically investigated by scholars (Towse et al., 2017; Barlow et al., 2022).75

What problems does it solve?

Antibiotic subscription models can be used to hinder the spread of antimicrobial resistance (AMR), which is partly driven by two factors:

- A volume-driven revenue model contributes to overprescription of antibiotics, which fuels AMR,76

- Due to a decay of existing antibiotics,77 new antibiotics need to be developed continuously. However, there is too little innovation in the field of antibiotics and “the pipeline of truly novel drugs in development or coming to market has dried up”. (Boluarte & Schulze, 2022, p. 6).

- Reduce the spread of AMR by preventing (or reducing) the incentives for overprescription of antibiotics

- Increase pharmacological innovation by providing financial predictability and security to developers in terms of their revenues

- Increase access to antibiotics as fixed payments are “in return for a sufficient antimicrobial product supply guarantee”

How is it implemented?

Two pilot programs in the UK and in Sweden that are currently being implemented have several differences: “Sweden’s intent to contract for all relevant antibiotics is a notable difference from the UK pilot’s intent to run a subscription model for just two drugs. […] Further, the main goal with the Swedish model is not to stimulate R&D but for now simply to guarantee access” (Rex, 2020).

When is it suitable?

While one interviewee suggested it may be feasible to implement a subscription model in LMICs, another was skeptical about the applicability of antibiotic subscription models to LMIC contexts.78

How commonly is it used?

We are aware of two subscription models currently being piloted, one in the UK (Cookson, 2022),79 and one in Sweden (Rex, 2020). The UK’s pilot program is currently under consideration for an expansion (Silverman Bonnifield & Towse, 2022). The PASTEUR Act (Pioneering Antimicrobial Subscriptions to End Up surging Resistance) has been proposed in the US Congress (Dall, 2022), and the European Union, Canada, and Japan are also considering introducing subscription models (Klemperer et al., 2022; Silverman Bonnifield & Towse, 2022). Relatedly, Charity Entrepreneurship recently announced advocacy for antibiotic subscription models as one of their top charity ideas for 2023 (Thompson, 2023). Moreover, staff at the Center for Global Development estimated the returns on investment of implementing large-scale antibiotic subscription programs in several countries and found that “the details are wonky, but the message is clear: new antibiotics are a terrific investment for all G7 members—and we look forward to Japan’s leadership under its G7 Presidency to make this vision a reality” (Silverman Bonnifield & Towse, 2022).80